Chapter 12 Financial Management and Financial Objectives

LEARNING OBJECTIVES 1. Explain the nature of financial management. |

1. The Nature and Purpose of Financial Management

1.1 |

Nature of Financial Management |

|

a. Financial management – can be defined as the management of the finances of an organization in order to achieve the financial objectives of the organization. The usual assumption in financial management for the private sector is that the objective of the company is to maximize shareholders’ wealth. |

1.2 The financial manager makes decisions relating to investment, financing and dividends. The management of risk must also be considered.

1.3 Investments in assets must be financed somehow. Financial management is also concerned with the management of short-term funds and with how funds can be raised over the long term.

1.4 The retention of profits is a financing decision. The other side of this decision is that if profits are retained, there is less to pay out to shareholders as dividends, which might deter investors. An appropriate balance needs to be struck in addressing the dividend decision.

1.5 Examples of different types of investment decision:

Decisions internal to the business enterprise |

|

Decision involving external parties |

|

Disinvestment decisions |

|

1.6 The statement of financial position and financial management:

2. Financial Management, Management Accounting and Financial Accounting

2.1 Management accounting

Financial management is mainly concerned with making decisions for the long-term future of the company. It involves making forecasts for the future and needs much external information (e.g. knowledge of competitors). The purpose is to make decisions which end up achieving the objectives of the company.

Once the long term decisions have been made, they need to be implemented and controlled. This is management accounting.

(a) Management accounting involves making short-term decisions as to how to implement the long-term strategy and involves the setting up of a control system in order to measure how well objectives are being achieved in order that corrections may be made if necessary.

(b) It tends to be short-term, and involves both past information and forecasts for the future.

2.2 Financial accounting => for past performance

(a) Financial accounting is the reporting to stakeholders – primarily shareholders – of how the company has performed and therefore effectively how well the financial manager and management accountant are doing their jobs.

(b) The financial accountant is fulfilling a legal requirement to report the profits, and it is not their role to look for ways of performing better – that is the job of the financial manager.

(c) The financial accountant is only looking at past information and information internal to the company.

3. Financial Objectives and Organizational Strategy

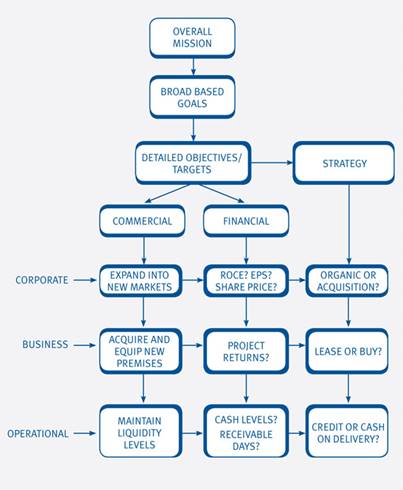

3.1 The financial manager needs to decide on strategies for the raising of finance, for the investment of capital, and for the management of working capital. However, before he can decide on these strategies he needs to identify what the objectives of the company are.

3.2 The following diagram is the key to understanding how financial management fits into overall business strategy.

3.3 The distinction between 'commercial' and 'financial' objectives is to emphasise that not all objectives can be expressed in financial terms and that some objectives derive from commercial marketplace considerations.

3.4 |

Shareholder Wealth Maximization (Dec 09) |

|

(a) Most companies are owned by shareholders and originally set up to make money for those shareholders. The primary objective of most companies is thus to maximise shareholder wealth. (This could involve increasing the share price and/or dividend payout.) |

3.5 Maximising and satisficing

One problem for the financial manager is to satisfy the objectives of several stakeholders at the same time. For example, reducing wages might increase profits and might satisfy shareholders, but would be unlikely to satisfy employees. Therefore, in practice a distinction must be made between maximising and satisficing.

(a) Maximising – seeking the best possible outcome

(b) Satisficing – finding a merely adequate outcome.

4. Objectives in Not-for-profit Organizations

4.1 Not-for-profit organizations include organizations such as charities, state health service and police force, where they are not run to make profits, but to provide a benefit.

4.2 Although good financial management of these organizations is important, it is not possible to have financial objectives of the same form as for companies. The focus therefore for these organizations is on value for money, i.e. attempting to get the maximum benefits for the least cost.

4.3 Value for money can be defined as getting the best possible combination of services from the least resources, which means maximising the benefits for the lowest possible cost.

4.4 This is usually accepted as requiring the application of economy, effectiveness and efficiency.

4.5 Economy is attaining the appropriate quantity and quality of inputs at lowest cost to achieve a certain level of outputs.

For example, the economy with which a school purchases equipment can be measured by comparing actual costs with budgets, with costs in previous years, with government/ local authority guidelines or with amounts spent by other schools.

4.6 Effectiveness is the extent to which declared objectives/goals are met.

For example, the effectiveness of a school's objective to produce quality teaching could be measured by the proportion of students going on to higher or further education.

4.7 Efficiency is the relationship between inputs and outputs.

For example, the efficiency with which a school's IT laboratory is used might be measured in terms of the proportion of the school week for which it is used.

5. Stakeholders

(Dec 11, Dec 15)

5.1 Although the theoretical objective of a private sector company might be to maximize the wealth of its owners, other individuals and groups have an interest in what a company does and they might be able to influence its corporate objectives. Anyone with an interest in the activities or performance of a company are ‘stakeholders’ because they have a stake or interest in what happens.

5.2 It is usual to group stakeholders into categories, with each category having its own interests and concerns. The main categories of stakeholder group in a company are usually the following.

Internal:

(a) Directors

(b) Employees

Connected:

(c) Shareholders

(d) Lenders

(e) Customers

(f) Suppliers

(g) Labour union

External:

(h) Government

(i) Society as a whole

5.3 The influence of the various stakeholders results in many firms adopting non-financial objectives in addition to financial ones. For example,

(a) Maintaining a contented workforce

(b) Showing respect for the environment

(c) Providing a top quality service to custoemrs

5.4 Goal incongruence between stakeholders (Dec 09)

For example, bondholders look for stable income in the form of interest and secured repayment of principal. Shareholders, on the other hand, look for increasing dividends and thus an increasing share price. The former do not prefer risky projects while the latter do not object to risky projects as the higher the risk, the higher the return. This illustrates the goal incongruence between bondholders and shareholders.

6. Agency Problem

(Dec 15)

6.1 Agency problem refers to the conflict of interests between various stakeholders of a company such as between shareholders and bondholders or between employees and shareholders. They arise in several ways.

(a) Moral hazard – A manager has an interest in receiving benefits from his or her position as a manager. These include all the benefits that come from status, such as a company car, use of a company airplane, lunches, and so on.

(b) Effort level – Managers may work less hard than they would if they were the owners of the company. The problem will exist in a large company at middle levels of management as well as senior management level.

(c) Earnings retention – The remuneration of directors and senior managers is often related to the size of the company, rather than its profits. Management are more likely to want to re-invest profits in order to make the company bigger, rather than payout the profits as dividends.

(d) Risk aversion – Executive directors and senior managers usually earn most of their income from the company they work for. They are therefore interested in the stability of the company, because this will protect their job and their future income. This means that management might be risk-averse, and reluctant to invest in higher-risk projects.

(e) Time horizon – Shareholders concern about the long-term financial prospects of their company, because the value of their shares depends on expectations for the long-term future. In contrast, managers might only be interested in the short-term. This is partly because they might receive annual bonuses based on short-term performance, and partly because they might not expect to be with the company for more than a few years.

6.2 Agency costs include direct and indirect costs.

(a) Direct costs include remuneration and audit fees.

(b) Indirect costs include the cost of lost opportunity because of agency problems.

6.3 Reducing the agency problem – Several methods of reducing the agency problem have been suggested. These include:

(a) Devising a remuneration package for executive directors and senior managers that gives them an incentive to act in the best interests of the shareholders. For example, one way to encourage managers to act in ways that increase shareholder wealth is to offer them share options. Share options will encourage managers to make decisions that are likely to lead to share price increases (such as investing in projects with positive net present values), since this will increase the rewards they receive from share options.

(b) Having enough independent non-executive directors inside the board. They have no executive role in the company and are not full-time employees. They are able to act in the best interests of the shareholders.

(c) Independent non-executive directors should also take the decisions where there is (or could be) a conflict of interest between executive directors and the best interests of the company. For example, non-executive directors should be responsible for the remuneration packages for executive directors and other senior managers.

(d) The threat of hostile takeover. If the corporation is badly managed, its share price will be low relative to its potential value. Competing management teams will be more likely to launch a hostile takeover when the share price is low. Typically the incumbent management will be fired. Therefore, managers have strong incentives to maximize share prices.

6.4 Incentive schemes (management reward schemes)

The structure of a remuneration package for executive directors or senior managers can vary, but it is usual for a remuneration package to have at least three elements.

(a) A basic salary – it needs to be high enough to attract and retain individuals with the required skills and talent.

(b) Annual performance incentives – The performance target might be stated as profit or earnings growth, EPS growth, achieving a profit target, etc. Some managers might also have a non-financial performance target.

(c) Long-term performance incentives – Which are linked in some way to share price growth. Long term incentives are usually provided in the form of share awards or share options of the company.

7. Corporate Governance

7.1 |

Corporate Governance (Dec 11) |

|

Corporate governance is the set of processes, customs, policies, laws, and institutions concerning the way a corporation (or company) is directed, administered or controlled. Corporate governance deals with the relationships among the stakeholders involved and the goals for which the corporation is governed. |

7.2 There are a number of key elements in corporate governance:

(a) The management and reduction of risk is a fundamental issue in all definitions of good governance; whether explicitly stated or merely implied.

(b) The notion that overall performance enhanced by good organisational structures and management practice within set best practice guidelines underpins most definitions.

(c) Good governance provides a framework for an organisation to pursue its strategy in an ethical and effective way from the perspective of all stakeholder groups affected, and offers safeguards against misuse of resources, physical or intellectual.

(d) Good governance is not just about externally established codes, it also requires a willingness to apply the spirit as well as the letter of the law.

(e) Accountability is generally a major theme in all governance frameworks.

7.3 Corporate governance codes of good practice generally cover the following areas:

(Jun 12)

(a) The board should be responsible for taking major policy and strategic decisions.

(b) Directors should have a mix of skills and their performance should be assessed regularly.

(c) Appointments should be conducted by formal procedures administered by a nomination committee (or selection committee).

(d) Division of responsibilities at the head of an organisation is most simply achieved by separating the roles of chairman and chief executive.

(e) Independent non-executive directors have a key role in governance. Their number and status should mean that their views carry significant weight.

(f) Directors' remuneration should be set by a remuneration committee consisting of independent non-executive directors.

(g) Remuneration should be dependent upon organisation and individual performance.

(h) Accounts should disclose remuneration policy and (in detail) the packages of individual directors.

(i) Boards should regularly review risk management and internal control, and carry out a wider review annually, the results of which should be disclosed in the accounts.

(j) Audit committees of independent non-executive directors should liaise with external auditors, supervise internal audit, and review the annual accounts and internal controls.

(k) The board should maintain a regular dialogue with shareholders, particularly institutional shareholders. The annual general meeting is a significant forum for communication.

(l) Annual reports must convey a fair and balanced view of the organisation. This might include whether the organisation has complied with governance regulations and codes, and give specific disclosures about the board, internal control reviews, going concern status and relations with stakeholders.

7.4 Triple bottom line (TBL) (Jun 13, Dec 13, Dec 15)

TBL is a metric in measuring economic value, social responsibility (people) and environmental responsibility (planet) for sustainability in business practice and development. It proposes to drop the financial bottom line as a meaningful indicator but replace it by social and environmental dimensions.

Examination Style Questions

Question 1

At a recent board meeting of Dartig Co, a non-executive director suggested that the company’s remuneration committee should consider scrapping the company’s current share option scheme, since executive directors could be rewarded by the scheme even when they did not perform well. A second non-executive director disagreed, saying the problem was that even when directors acted in ways which decreased the agency problem, they might not be rewarded by the share option scheme if the stock market were in decline.

Required:

Explain the nature of the agency problem and discuss the use of share option schemes as a way of reducing the agency problem in a stock-market listed company such as Dartig Co.

(8 marks)

(ACCA F9 Financial Management December 2008 Q1(e))

Question 2

Discuss the relationship between investment decisions, dividend decisions and financing decisions in the context of financial management, illustrating your discussion with examples where appropriate. (8 marks)

(ACCA F9 Financial Management June 2010 Q4(c))

Question 3

Mrs Vanessa Wong operates a very successful retailing business in Hong Kong. Over the years, she has established five retail shops on Hong Kong Island, in Kowloon and in the New Territories. With economic recovery well under way, she plans to expand the local business; in addition, she is also considering penetrating the Chinese mainland market in order to capitalize on the ever-increasing purchasing power of Chinese consumers. Although she is financially healthy, Vanessa feels her current financial resources may not be adequate for the planned expansion. She would like to explore alternative business organization forms and has asked you to address the following list of questions.

Required:

(a) What is the primary goal of a corporation? Why? (3 marks)

(b) What is an agency relationship? What is the agency problem in a corporation? (3 marks)

(c) Describe THREE mechanisms that can encourage managers to behave in the best interest of shareholders. (5 marks)

(HKIAAT PBE Paper III Financial Management June 2003 Q1(c), (d) & (e))

Question 4

Ms Lily Gong, Chairwoman of Fortune Garment Manufacturing Ltd, made this statement in the company’s annual report: “Our goal is stock price maximization for our shareholders.”

Required:

(a) What is the difference between stock price maximization and profit maximization?

(5 marks)

(b) What actions can shareholders take to ensure that management’s interests are the same as those of shareholders? (5 marks)

(HKIAAT PBE Paper III Financial Management December 2004 Q6(a)(i) & (ii))

Question 5

A financial manager chats with a shareholder in an annual general meeting. “Although maximization of shareholder wealth is, in theory, more appropriate than maximization of profit as the goal of the firm, it can never be achieved in the real world because of market inefficiency and agency problem.”

Required:

(a) Explain and contrast the two alternative goals of the firm, namely, maximization of shareholder wealth and maximization of profit. (5 marks)

(b) Explain the concept of market efficiency and its various forms. What form of market efficiency would be performed by financial managers and by shareholders respectively to achieve the goal of maximization shareholders wealth? Why? (5 marks)

(c) Explain agency problems from the point of view of shareholders. Are there any ethical problems involved? (5 marks)

(d) Do you agree with the remark of the financial manager? Why? (5 marks)

(Total 20 marks)

(HKIAAT PBE Paper III Financial Management June 2007 Q5)

Question 6

Required:

(a) What should be minimum or breakeven price charged for a normal attendance night?

(5 marks)

(b) In reality, the actual prices are different from the result calculated in (a). What are the reasons for that? (5 marks)

(c) “The goal of a company is to maximize shareholders’ wealth, not to maximize profit.” Discuss this statement. (6 marks)

(d) Why is there normally no goal congruence between bondholders and shareholders?

(4 marks)

(HKIAAT PBE Paper II Management Accounting and Finance December 2009 Q4)

Question 7

“A Company has many stakeholders. Managing a company is never an easy task” said by a chief executive officer of a company.

Required:

(a) By using an accounting equation, identify two groups of stakeholders of a company and their returns. (4 marks)

(b) In times of economic downturn, explain why there are conflicts of interest between the stakeholders mentioned in part (a). (4 marks)

(c) Other than the stakeholders mentioned in part (a), why does management/managers also create conflicts of interest with these stakeholders? (4 marks)

(d) Suggest TWO ways of resolving the conflicts of interest mentioned in part (b) and (c).

(6 marks)

(e) What is corporate governance? Explain briefly. (2 marks)

(HKIAAT PBE Paper II Management Accounting and Finance December 2011 Q4)

Question 8

Explain the meaning and significance of the three components of the Triple Bottom Line.

(3 marks)

(HKIAAT PBE Paper II Management Accounting and Finance June 2013 Q2(c))

Question 9

Triple Bottom Line is a popular method in evaluating non-financial performance. Explain what Tripe Bottom Line is. (6 marks)

(HKIAAT PBE Paper II Management Accounting and Finance December 2013 Q5(e))

Question 10

Beside financial performance, companies may make use of Triple Bottom Line in their evaluation. Explain TWO aspects of the Triple Bottom Line with respect to this private school case, and provide one example for each aspect. (6 marks)

(HKIAAT PBE Paper II Management Accounting and Finance December 2015 Q3(e))

Question 11

Tunnel Company is a tunnel management company which has been running at a loss of many years. Recently, it cannot pay salaries to employees on time. For example, the salary payment for December can only be settled in early February next year. If the situation continues, the license of Tunnel Company may be revoked by the government.

Required:

(a) Suggest TWO possible ways to tackle the anticipated financial distress problem of Tunnel Company. (4 marks)

(b) Name FOUR stakeholders involved in this case. (4 marks)

(c) Based on the answer in part (b), describe the types of returns earned by these FOUR stakeholders. (4 marks)

(d) What is agency problem relating to a company? (4 marks)

(e) Give TWO examples of agency costs. (4 marks)

(HKIAAT PBE Paper II Management Accounting and Finance December 2015 Q5)

Source: https://hkiaatevening.yolasite.com/resources/PBEP2Notes/Chapter12-FMandObj.doc

Web site to visit: https://hkiaatevening.yolasite.com

Author of the text: indicated on the source document of the above text

If you are the author of the text above and you not agree to share your knowledge for teaching, research, scholarship (for fair use as indicated in the United States copyrigh low) please send us an e-mail and we will remove your text quickly. Fair use is a limitation and exception to the exclusive right granted by copyright law to the author of a creative work. In United States copyright law, fair use is a doctrine that permits limited use of copyrighted material without acquiring permission from the rights holders. Examples of fair use include commentary, search engines, criticism, news reporting, research, teaching, library archiving and scholarship. It provides for the legal, unlicensed citation or incorporation of copyrighted material in another author's work under a four-factor balancing test. (source: http://en.wikipedia.org/wiki/Fair_use)

The information of medicine and health contained in the site are of a general nature and purpose which is purely informative and for this reason may not replace in any case, the council of a doctor or a qualified entity legally to the profession.

The texts are the property of their respective authors and we thank them for giving us the opportunity to share for free to students, teachers and users of the Web their texts will used only for illustrative educational and scientific purposes only.

All the information in our site are given for nonprofit educational purposes