Chapter 9 Working Capital Management – Inventory, Accounts Receivable and Payable

1. Objectives

1.1 Explain the objective of inventory management.

1.2 Define and explain lead time and buffer inventory.

1.3 Explain and apply the basic economic order quantity (EOQ) formula to data provided.

1.4 Calculate the EOQ taking account of quantity discounts and calculate the financial implications of discounts for bulk purchases.

1.5 Define and calculate the re-order level where demand and lead time are known.

1.6 Describe and evaluate the main inventory management systems including Just-In-time (JIT) techniques.

1.7 Explain how to establish and implement a credit policy for accounts receivable.

1.8 Explain the administration involved in collecting amounts owing from accounts receivable

1.9 Explain the pros and cons of offering discounts for early settlement.

1.10 Define and explain the features of factoring and invoice discounting.

1.11 Explain the factors involved in the effective management of accounts payable.

1.12 Explain the specific factors to be considered when managing foreign trade.

Summary

2. Managing Inventories

2.1 Costs of inventories

2.1.1 Inventory is a major investment for many companies. Manufacturing companies can easily be carrying inventory equivalent to between 50% and 100% of the revenue of the business. It is therefore essential to reduce the levels of inventory held to the necessary minimum.

2.1.2 |

Costs of High Inventory Levels |

|

Keeping inventory levels high is expensive owing to: |

2.1.3 Carrying inventory involves a major working capital investment and therefore levels need to be very tightly controlled. The cost is not just that of purchasing the goods, but also storing, insuring, and managing them once they are in inventory.

2.1.4 Purchase costs: once goods are purchased, capital is tied up in them and until sold on (in their current state or converted into a finished product), the capital earns no return. This lost return is an opportunity cost of holding the inventory.

2.1.5 Stores administration: in addition, the goods must be stored. The company must incur the expense of renting out warehouse space, or if using space they own, there is an opportunity cost associated with the alternative uses the space could be put to. There may also be additional requirements such as controlled temperature or light which require extra funds.

2.1.6 Other risks: once stored, the goods will need to be insured. Specialist equipment may be needed to transport the inventory to where it is to be used. Staff will be required to manage the warehouse and protect against theft and if inventory levels are high, significant investment may be required in sophisticated inventory control systems.

2.1.7 The longer inventory is held, the greater the risk that it will deteriorate or become out of date. This is true of perishable goods, fashion items and high-technology products, for example.

2.1.8 |

Costs of Low Inventory Levels |

|

If inventory levels are kept too low, the business faces alternative problems: |

2.1.9 Stockout: if a business runs out of a particular product used in manufacturing it may cause interruptions to the production process – causing idle time, stockpiling of work-in-progress (WIP) or possibly missed orders. Alternatively, running out of goods held for onward sale can result in dissatisfied customers and perhaps future lost orders if custom is switched to alternative suppliers. If a stockout looms, the business may attempt to avoid it by acquiring the goods needed at short notice. This may involve using a more expensive or poorer quality supplier.

2.1.10 Re-order/setup costs: each time inventory runs out, new supplies must be acquired. If the goods are bought in, the costs that arise are associated with administration – completion of a purchase requisition, authorisation of the order, placing the order with the supplier, taking and checking the delivery and final settlement of the invoice. If the goods are to be manufactured, the costs of setting up the machinery will be incurred each time a new batch is produced.

2.1.11 Lost quantity discounts: purchasing items in bulk will often attract a discount from the supplier. If only small amounts are bought at one time in order to keep inventory levels low, the quantity discounts will not be available.

2.1.12 |

The Objective of Good Inventory Management |

|

The objective of good inventory management is therefore to determine: |

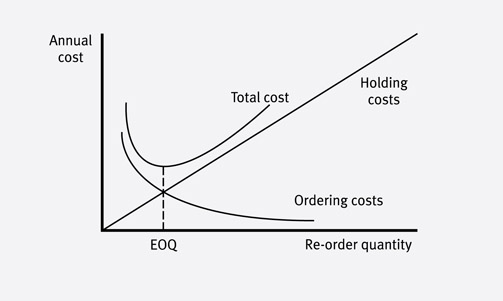

2.2 Economic Order Quantity (EOQ)

(Dec 07, Jun 08, Dec 10)

2.2.1 For businesses that do not use JIT (discussed in more detail below), there is an optimum order quantity for inventory items, known as the EOQ.

2.2.2 The aim of the EOQ model is to minimise the total cost of holding and ordering inventory.

2.2.3 |

EOQ Formula |

|

EOQ = |

2.2.4 |

Example 1 |

|

The demand for a commodity is 40,000 units a year, at a steady rate. It costs $20 to place an order, and 40 cents to hold a unit for a year. Find the order size to minimize inventory costs, the number of orders placed each year, the length of the inventory cycle and the total costs of holding inventory for the year. Solution: EOQ = |

2.2.5 Limitations of EOQ

(a) Only based on two types of costs: holding costs and ordering costs.

(b) Demand for stock, holding cost per unit per year and order cost are assumed to be certain and constant.

(c) Ignore the cost of running out of stock (stockouts).

(d) Developed on the basis of zero lead time and no buffer stock.

2.3 Quantity discounts

(Jun 11, Dec 12)

2.3.1 Discounts may be offered for ordering in large quantities. If the EOQ is smaller than the order size needed for a discount, should the order size be increased above the EOQ?

2.3.2 |

Example 2 |

||||||||||||||||||||||||||||||

|

The annual demand for an item of inventory is 125 units. The item costs $200 a unit to purchase, the holding cost for one unit for one year is 15% of the unit cost and ordering costs are $300 an order. The supplier offers a 3% discount for order of 60 units or more, and a discount of 5% for orders of 90 units or more. What is the cost minimizing order size? Solution: (a) The EOQ ignoring discount is:

(b) With a discount of 3% and an order quantity of 60 units costs are as follows.

(c) With a discount of 5% and an order quantity of 90 units costs are as follows.

The cheapest option is to order 90 units at a time. |

2.3.3 |

Test your understanding 1 |

||||||||||

|

A company uses an item of inventory as follows.

Should the company order 1,000 units at a time in order to secure an 8% discount? |

2.4 Re-order level (ROL)

2.4.1 Having decided how much inventory to re-order, the next problem is when to re-order. The firm needs to identify a level of inventory which can be reached before an order needs to be placed.

2.4.2 When lead time and demand are known with certainty, ROL = demand during lead time. Where there is uncertainty, an optimum level of buffer inventory must be found.

2.4.3 If an order is placed too late, the organization may run out of inventory, a stock-out, resulting in a loss of sales and/or a loss of production.

2.4.4 If an order is placed too soon, the organization will hold too much inventory, and inventory holding costs will be excessive.

2.4.5 |

Re-order Level Formula |

|

Re-order level = maximum usage x maximum lead time Lead time – the lag between when an order is placed and the item is delivered. Use of a re-order level builds in a measure of safety inventory and minimizes the risk of the organization running out of inventory. This is particularly important when the volume of demand or the supply lead time are uncertain.

|

2.5 Maximum and minimum inventory levels

2.5.1 |

Formula |

|

Maximum inventory level = Minimum inventory level or buffer safety inventory = Average inventory = minimum level + re-order level / 2 |

2.5.2 The maximum level acts a warning signal to management that inventories are reaching a potentially wasteful level.

2.5.3 The minimum level acts as a warning to management that inventories are approaching a dangerously low level and that stock-outs are possible.

2.5.4 Under average inventory, it assumes that inventory levels fluctuate evenly between the minimum (or safety) inventory level and the highest possible inventory level.

2.5.5 This approach assumes that a business wants to minimize the risk of stock-outs at all costs. In the modern manufacturing environment stock-outs can have a disastrous effect on the production process.

2.6 Inventory management systems – Just-in-time (JIT)

2.6.1 |

JIT |

|

JIT is a series of manufacturing and supply chain techniques that aim to minimise inventory levels and improve customer service by manufacturing not only at the exact time customers require, but also in the exact quantities they need and at competitive prices. JIT procurement is a term which describes a policy of obtaining goods from suppliers at the latest possible time (i.e. when they are needed) and so avoiding the need to carry any materials or components inventory. |

2.6.2 |

Benefits of JIT (Dec 10) |

|

(a) Reduction in inventory holding costs |

2.6.3 JIT will not be appropriate in some cases. For example, a restaurant might find it preferable to use the traditional EOQ approach for staple non-perishable food inventories but adopt JIT for perishable and exotic items. In a hospital, a stock-out could quite literally be fatal and so JIT would be quite unsuitable.

3. Managing Accounts Receivable

3.1 Cost of financing receivables

3.1.1 Management must establish a credit policy. The optimum level of trade credit extended represents a balance between two factors:

(a) profit improvement from sales obtained by allowing credit

(b) the cost of credit allowed.

3.1.2 A firm must establish a policy for credit terms given to its customers. Ideally the firm would want to obtain cash with each order delivered, but that is impossible unless substantial settlement (or cash) discounts are offered as an inducement. It must be recognised that credit terms are part of the firm’s marketing policy. If the trade or industry has adopted a common practice, then it is probably wise to keep in step with it.

3.1.3 A lenient (寬大的) credit policy may well attract additional customers, but at a disproportionate increase in cost.

3.1.4 |

Four Key Aspects of a Credit Policy (Pilot, Dec 07, Jun 10, Jun 13) |

|

(a) Assess creditworthiness. |

3.1.5 |

Example 3 |

|

Paisley Co has sales of $20 million for the previous year, receivables at the year end were $4 million, and the cost of financing receivables is covered by an overdraft at the interest rate of 12% pa. Required: (a) calculate the receivables days for Paisley Solution: (a) Receivables days = $4m ÷ $20m × 365 = 73 days |

3.2 Assessing creditworthiness

3.2.1 A firm should assess the creditworthiness of:

(a) all new customers immediately

(b) existing customers periodically.

3.2.2 Credit control involves the initial investigation of potential customers and continuing control of outstanding accounts. The main points to note are as follows:

(a) New customers should give good references, including one from a bank, before being granted credit, or credit reference agencies such as Dunn & Bradstreet publish general financial details of many companies, together with a credit rating.

(b) Credit ratings might be checked through a credit rating agency.

(c) A new customer’s credit limit should be fixed at a low level and only increased if his payment record subsequently warrants it.

(d) For large value customers, a file should be maintained of any available financial information about the customer. This file should be reviewed regularly. Information is available from, for example, an analysis of the company’s annual report and accounts.

(e) Press comments may give information about what a company is currently doing.

(f) The company could send a member of staff to visit the company concerned, to get a first-hand impression of the company and its prospects. This would be advisable in the case of a prospective major customer.

3.3 Credit policy

3.3.1 |

Regular Monitoring |

|

Regular monitoring of accounts receivables is very important. Individual accounts receivables can be assessed using a customer history analysis (i.e. aging report) and a credit rating system. The overall level of accounts receivable can be monitored using an aged accounts receivable listing and credit utilization report, as well as reports on the level of bad debts. |

3.3.2 |

Credit Utilisation Report |

||||||||||||||||||||||||||||||||

|

The total amount of credit offered, as well as individual accounts, should be policed to ensure that the senior management policy with regard to the total credit limits is maintained. A credit utilization report can indicate the extent to which total limits are being utilized. An example is given below.

This might also contain other information, such as days sales outstanding and so on. Reviewed in aggregate, this can reveal the following. |

3.3.3 Extension of credit – to determine whether it would be profitable to extend the level of total credit, it is necessary to assess:

(a) The extra sales that a more generous credit policy would stimulate.

(b) The profitability of the extra sales.

(c) The extra length of the average debt collection period.

(d) The required rate of return on the investment in additional accounts receivable.

3.3.4 |

Example 4 – A change in credit policy |

||||||||||||||||||||||||||||||||||||||||

|

ABC Co is considering a change of credit policy which will result in an increase in the average collection period from one to two months. The relaxation in credit is expected to produce an increase in sales in each year amounting to 25% of the current sales volume.

The required rate of return on investments is 20%. Assume that the 25% increase in sales would result in additional inventories of $100,000 and additional accounts payable of $20,000. Advise the company on whether or not to extend the credit period offered to customers, if: Solution: The change in credit policy is justifiable if the rate of return on the additional investment in working capital would exceed 20%.

(a) Extra investment, if all accounts receivable take two months credit

Return on extra investment = $90,000 / $380,000 = 23.7% (b) Extra investment, if only the new accounts receivable take two months credit

Return on extra investment = $90,000 / $180,000 = 50% In both case (a) and case (b) the new credit policy appears to be worthwhile. |

3.3.5 |

Test Your Understanding 2 |

|

ABC Co currently expects sales of $50,000 a month. Variable costs of sales are $40,000 a month (all payable in the month of sales). It is estimated that if the credit period allowed to accounts receivable were to be increased from 30 days to 60 days, sales volume would increase by 20%. All customers would be expected to take advantage of the extended credit. If the cost of capital is 12.5% a year (or approximately 1% a month), is the extension of the credit period justifiable in financial terms? |

3.4 Collecting overdue debts

3.4.1 A credit period only begins once an invoice is received so prompt invoicing is essential. If debts go overdue, the risk of default increases, therefore a system of follow-up procedures is required:

3.5 Early settlement discounts

(Dec 10, Dec 12)

3.5.1 |

Key Points |

|

(a) Early settlement discounts are given to encourage early payment by customers. The cost of the discount is balanced against the savings the company receives from having less capital tied up due to a lower receivables balance and a shorter average collection period. Discounts may also reduce the number of irrecoverable debts. (b) The benefit in interest cost saved should exceed the cost of the discounts allowed. |

3.5.2 Advantages and disadvantages of offering early settlement discounts:

Advantages |

Disadvantages |

(a) Early payment reduces the receivables balance and hence the finance costs. |

(a) Difficulty in setting the appropriate terms. |

3.5.3 |

Example 5 |

|

A company offers its goods to customers on 30 days’ credit, subject to satisfactory trade references. It also offers a 2% discount if payment is made within ten days of the date of the invoice. Required: Calculate the cost to the company of offering the discount, assuming a 365 day year. Solution: Discount as a percentage of amount paid = 2 / 98 = 2.04%. |

3.5.4 |

Test Your Understanding 3 |

|

A company is offering a cash discount of 2.5% to receivables if they agree to pay debts within one month. The usual credit period taken is three months. What is the effective annualized cost of offering the discount and should it be offered, if the bank would loan the company at 18% pa? |

4. Factoring and Invoicing Discounting

4.1 Factoring

4.1.1 Factoring (應收帳款承購業務) and invoice discounting (發票貼現) are both ways of speeding up the receipt of funds from accounts receivable. This improves cash flow and liquidity.

4.1.2 |

Factoring (Jun 08) |

|

Factoring is the outsourcing of the credit control department to a third party. The debts of the company are effectively sold to a factor (normally owned by a bank). The factor takes on the responsibility of collecting the debt for a fee. The company can choose some or all of the following three services offered by the factor: |

4.1.3 Factoring is most suitable for:

(a) small and medium-sized firm which often cannot afford sophisticated credit and sales accounting systems, and

(b) firms that are expanding rapidly. These often have a substantial and growing investment in inventory and receivables, which can be turned into cash by factoring the debts. Factoring debts can be a more flexible source of financing working capital than an overdraft or bank loan.

4.1.4 Factoring can be arranged on either a ‘without recourse” basis or a “with recourse” basis.

(a) When factoring is without recourse or ‘non-recourse’, the factor provides protection for the client against irrecoverable debts. The factor has no ‘comeback’ or recourse to the client if a customer defaults. When a customer of the client fails to pay a debt, the factor bears the loss and the client receives the money from the debt.

(b) When the service is with recourse (‘recourse factoring’), the client must bear the loss from any irrecoverable debt, and so has to reimburse the factor for any money it has already received for the debt.

(c) Credit protection is provided only when the service is non-recourse and this is obviously more costly.

4.1.5 Typical factoring arrangements

(a) Administration and debt collection

(b) Including financing

4.1.6 Advantages and disadvantages of factoring

(Dec 11)

Advantages |

Disadvantages |

(a) Saving in administration costs – not incur the costs of running its own sales ledger department. |

(a) Likely to be more costly than an efficiently run internal credit control department. |

4.1.7 Determine whether factoring is financially acceptable

(Dec 08, Dec 11)

4.1.8 |

Example 6 |

||||||||||||||||||||||||||||||||||||||||

|

A company makes annual credit sales of $1,500,000. Credit terms are 30 days, but its debt administration has been poor and the average collection period has been 45 days with 0.5% of sales resulting in bad debts which are written off. A factor would take on the task of debt administration and credit checking, at an annual fee of 2.5% of credit sales. The company would save $30,000 a year in administration costs. The payment period would be 30 days. The factor would also provide an advance of 80% of invoiced debts at an interest rate of 14% (3% over the current base rate). The company can obtain an overdraft facility to finance its accounts receivable at a rate of 2.5% over base rate. Should the factor’s service be accepted? Assume a constant monthly turnover. Solution: It is assumed that the factor would advance an amount equal to 80% of the invoiced debts, and the balance 30 days later. (a) The current situation is as follows, using the company’s debt collection staff and a bank overdraft to finance all debts.

(b) The cost of the factor. 80% of credit sales financed by the factor would be 80% of $1,500,000 = $1,200,000. For a consistent comparison, we must assume that 20% of credit sales would be financed by a bank overdraft. The average credit period would be only 30 days. The annual cost would be as follows.

(c) Conclusion. The factor is cheaper. In this case, the factor’s fees exactly equal the savings in bad debts ($7,500) and administration costs ($30,000). The factor is then cheaper overall because it will be more efficient at collecting debts. The advance of 80% of debts is not needed, however, if the company has sufficient overdraft facility because the factor’s finance charge of 14% is higher than the company’s overdraft rate of 13.5%. An alternative way of carrying out the calculation is to consider the changes that using a factor will mean.

|

4.2 Invoice discounting

4.2.1 |

Invoice Discounting (Jun 08) |

|

Invoice discounting is a method of raising finance against the security of receivables without using the sales ledger administration services of a factor. With invoice discounting, the business retains control over its sales ledger, and confidentiality in its dealings with customers. Firms of factors will also provide invoice discounting to clients.

|

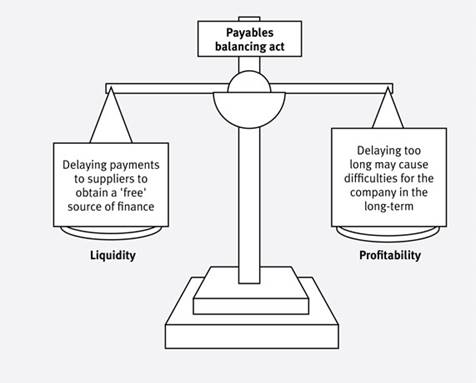

5. Management of Trade Accounts Payable

5.1 Trade credit is the simplest and most important source of short-term finance for many companies. Again it is a balancing act between liquidity and profitability.

5.2 By delaying payment to suppliers companies face possible problems:

(a) supplier may refuse to supply in future

(b) supplier may only supply on a cash basis

(c) there may be loss of reputation

(d) supplier may increase price in future.

5.3 Trade credit is normally seen as a ‘free’ source of finance. Whilst this is normally true, it may be that the supplier offers a discount for early payment. In this case delaying payment is no longer free, since the cost will be the lost discount.

5.4 |

Example 7 |

|

One supplier has offered a discount to Box Co of 2% on an invoice for $7,500, if payment is made within one month, rather than the three months normally taken to pay. If Box’s overdraft rate is 10% pa, is it financially worthwhile for them to accept the discount and pay early? Solution: Discount saves 2% of $7,500 = $150 Alternatively: |

6. Managing Foreign Trades

(Jun 09)

6.1 Overseas accounts receivable and payable bring additional risks that need to be managed:

(a) Export credit risk

(b) Foreign exchange risk

6.2 Export credit risk is the risk of failure or delay in collecting payments due from foreign customers. It may be caused by:

(a) insolvent customers

(b) bank failure

(c) unconvertible currencies

(d) political risk

6.3 Solutions include:

(a) using banks as intermediaries

(b) irrevocable letter of credit (ILC)

(c) acquiring guarantees

(d) taking out export cover

(e) good business management

6.4 Foreign exchange risk is a risk that the value of the currency will change between the date of the contract and the date of settlement. This will be discussed in later chapters

Examination Style Questions

Question 1

TNG Co expects annual demand for product X to be 255,380 units. Product X has a selling price of £19 per unit and is purchased for £11 per unit from a supplier, MKR Co. TNG places an order for 50,000 units of product X at regular intervals throughout the year. Because the demand for product X is to some degree uncertain, TNG maintains a safety (buffer) stock of product X which is sufficient to meet demand for 28 working days. The cost of placing an order is £25 and the storage cost for Product X is 10 pence per unit per year.

TNG normally pays trade suppliers after 60 days but MKR has offered a discount of 1% for cash settlement within 20 days.

TNG Co has a short-term cost of debt of 8% and uses a working year consisting of 365 days.

Required:

(a) Calculate the annual cost of the current ordering policy. Ignore financing costs in this part of the question. (4 marks)

(b) Calculate the annual saving if the economic order quantity model is used to determine an optimal ordering policy. Ignore financing costs in this part of the question. (5 marks)

(c) Determine whether the discount offered by the supplier is financially acceptable to TNG Co. (4 marks)

(d) Critically discuss the limitations of the economic order quantity model as a way of managing stock. (4 marks)

(e) Discuss the advantages and disadvantages of using just-in-time stock management methods. (8 marks)

(25 marks)

(ACCA 2.4 Financial Management and Control June 2005 Q5)

Question 2 – Changes of credit policy, Miller-Orr Model, AR management and working capital funding policy

Ulnad Co has annual sales revenue of $6 million and all sales are on 30 days’ credit, although customers on average take ten days more than this to pay. Contribution represents 60% of sales and the company currently has no bad debts. Accounts receivable are financed by an overdraft at an annual interest rate of 7%.

Ulnad Co plans to offer an early settlement discount of 1.5% for payment within 15 days and to extend the maximum credit offered to 60 days. The company expects that these changes will increase annual credit sales by 5%, while also leading to additional incremental costs equal to 0.5% of turnover. The discount is expected to be taken by 30% of customers, with the remaining customers taking an average of 60 days to pay.

Required:

(a) Evaluate whether the proposed changes in credit policy will increase the profitability of Ulnad Co. (6 marks)

(b) Renpec Co, a subsidiary of Ulnad Co, has set a minimum cash account balance of $7,500. The average cost to the company of making deposits or selling investments is $18 per transaction and the standard deviation of its cash flows was $1,000 per day during the last year. The average interest rate on investments is 5.11%. Determine the spread, the upper limit and the return point for the cash account of Renpec Co using the Miller-Orr model and explain the relevance of these values for the cash management of the company. (6 marks)

(c) Identify and explain the key areas of accounts receivable management.

(6 marks)

(d) Discuss the key factors to be considered when formulating a working capital funding policy. (7 marks)

(Total 25 marks)

(ACCA F9 Financial Management Pilot Paper Q3)

Question 3 – Working capital management, EOQ and hedging

PKA Co is a European company that sells goods solely within Europe. The recently-appointed financial manager of PKA Co has been investigating the working capital management of the company and has gathered the following information:

Inventory management

The current policy is to order 100,000 units when the inventory level falls to 35,000 units. Forecast demand to meet production requirements during the next year is 625,000 units. The cost of placing and processing an order is €250, while the cost of holding a unit in stores is €0·50 per unit per year. Both costs are expected to be constant during the next year. Orders are received two weeks after being placed with the supplier. You should assume a 50-week year and that demand is constant throughout the year.

Accounts receivable management

Domestic customers are allowed 30 days’ credit, but the financial statements of PKA Co show that the average accounts receivable period in the last financial year was 75 days. The financial manager also noted that bad debts as a percentage of sales, which are all on credit, increased in the last financial year from 5% to 8%.

Accounts payable management

PKA Co has used a foreign supplier for the first time and must pay $250,000 to the supplier in six months’ time. The financial manager is concerned that the cost of these supplies may rise in euro terms and has decided to hedge the currency risk of this account payable. The following information has been provided by the company’s bank:

Spot rate ($ per €): |

1.998 ± 0.002 |

Six months forward rate ($ per €): |

1.979 ± 0.004 |

Money market rates available to PKA Co:

|

Borrowing |

Deposit |

One year euro interest rates: |

6.1% |

5.4% |

One year dollar interest rates: |

4.0% |

3.5% |

Assume that it is now 1 December and that PKA Co has no surplus cash at the present time.

Required:

(a) Identify the objectives of working capital management and discuss the conflict that may arise between them. (3 marks)

(b) Calculate the cost of the current ordering policy and determine the saving that could be made by using the economic order quantity model. (7 marks)

(c) Discuss ways in which PKA Co could improve the management of domestic accounts receivable. (7 marks)

(d) Evaluate whether a money market hedge, a forward market hedge or a lead payment should be used to hedge the foreign account payable. (8 marks)

(Total 25 marks)

(ACCA F9 Financial Management December 2007 Q4)

Question 4 – Factoring, invoicing discounting and EOQ

FLG Co has annual credit sales of $4·2 million and cost of sales of $1·89 million. Current assets consist of inventory and accounts receivable. Current liabilities consist of accounts payable and an overdraft with an average interest rate of 7% per year. The company gives two months’ credit to its customers and is allowed, on average, one month’s credit by trade suppliers. It has an operating cycle of three months.

Other relevant information:

Current ratio of FLG Co 1·4

Cost of long-term finance of FLG Co 11%

Required:

(a) Discuss the key factors which determine the level of investment in current assets. (6 marks)

(b) Discuss the ways in which factoring and invoice discounting can assist in the management of accounts receivable. (6 marks)

(c) Calculate the size of the overdraft of FLG Co, the net working capital of the company and the total cost of financing its current assets. (6 marks)

(d) FLG Co wishes to minimise its inventory costs. Annual demand for a raw material costing $12 per unit is 60,000 units per year. Inventory management costs for this raw material are as follows:

Ordering cost: $6 per order

Holding cost: $0·5 per unit per year

The supplier of this raw material has offered a bulk purchase discount of 1% for orders of 10,000 units or more. If bulk purchase orders are made regularly, it is expected that annual holding cost for this raw material will increase to $2 per unit per year.

Required:

(i) Calculate the total cost of inventory for the raw material when using the economic order quantity. (4 marks)

(ii) Determine whether accepting the discount offered by the supplier will minimise the total cost of inventory for the raw material. (3 marks)

(Total 25 marks)

(ACCA F9 Financial Management June 2008 Q3)

Source: https://hkiaatevening.yolasite.com/resources/FMNotes/Chapter9-WCInventoryARAP.doc

Web site to visit: https://hkiaatevening.yolasite.com

Author of the text: indicated on the source document of the above text

If you are the author of the text above and you not agree to share your knowledge for teaching, research, scholarship (for fair use as indicated in the United States copyrigh low) please send us an e-mail and we will remove your text quickly. Fair use is a limitation and exception to the exclusive right granted by copyright law to the author of a creative work. In United States copyright law, fair use is a doctrine that permits limited use of copyrighted material without acquiring permission from the rights holders. Examples of fair use include commentary, search engines, criticism, news reporting, research, teaching, library archiving and scholarship. It provides for the legal, unlicensed citation or incorporation of copyrighted material in another author's work under a four-factor balancing test. (source: http://en.wikipedia.org/wiki/Fair_use)

The information of medicine and health contained in the site are of a general nature and purpose which is purely informative and for this reason may not replace in any case, the council of a doctor or a qualified entity legally to the profession.

The texts are the property of their respective authors and we thank them for giving us the opportunity to share for free to students, teachers and users of the Web their texts will used only for illustrative educational and scientific purposes only.

All the information in our site are given for nonprofit educational purposes